Best Home Equity Loans in 2026: HELOC vs Lump Sum, Rates and How to Qualify

Updated April 2026

American homeowners are sitting on roughly $17.6 trillion in home equity as of early 2026. That is an enormous amount of wealth locked up in real estate, and tapping it can make sense in certain situations. But it can also be a terrible idea if you are not careful. Your home is on the line, literally.

I spent two weeks comparing the major home equity lenders, talking to a mortgage broker friend, and running numbers through our HELOC calculator. Here is what I found, including the mistakes I see people making repeatedly.

Home Equity Loan vs HELOC vs Cash-Out Refinance

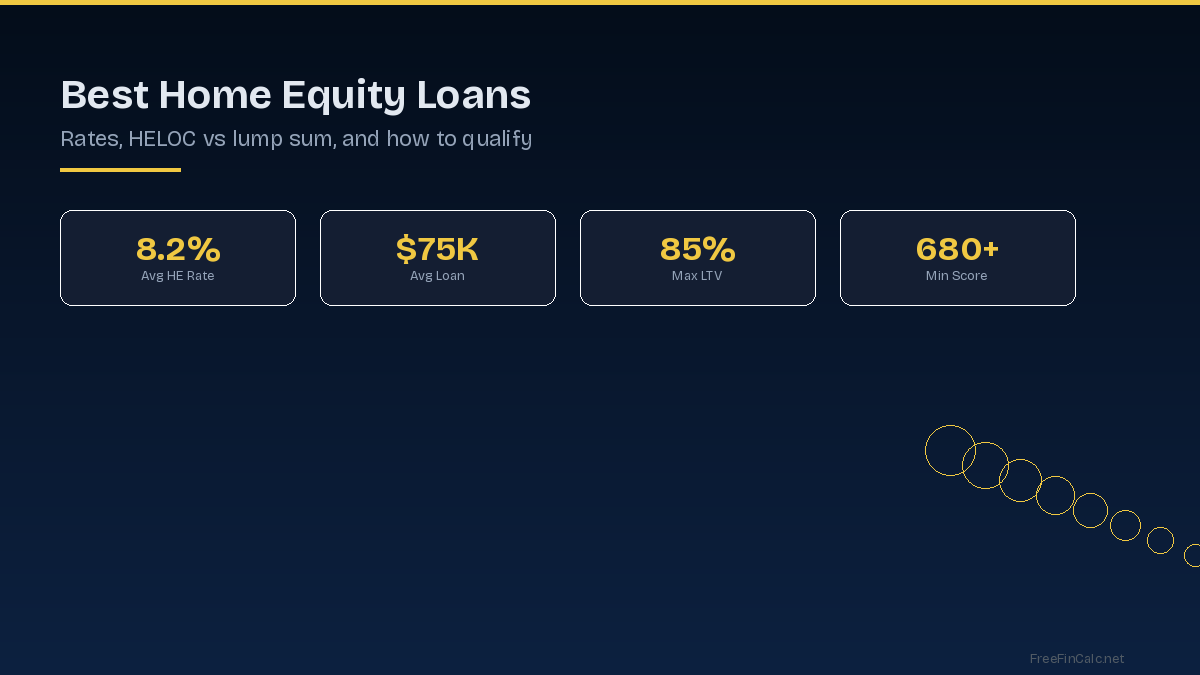

Three ways to access your equity, each with different trade-offs. A home equity loan gives you a lump sum with a fixed rate and fixed payments. Think of it as a second mortgage. Rates average around 8.2 percent in 2026. Best for one-time projects with a known cost, like a $50,000 kitchen renovation.

A HELOC works like a credit card secured by your home. You get a credit line and borrow as needed during a draw period of 5 to 10 years, paying interest only on what you use. Rates are variable, averaging 7.5 percent currently. Best for ongoing projects or when you are not sure exactly how much you will need.

A cash-out refinance replaces your entire mortgage with a larger one and gives you the difference in cash. Rates are around 6.8 percent. This only makes sense if your current mortgage rate is higher than today's rates, because otherwise you are refinancing into a worse rate on your entire mortgage balance just to access some equity.

How Much Can You Actually Borrow

Lenders use a metric called combined loan-to-value ratio (CLTV). Most cap it at 80 to 85 percent, meaning your total borrowing (first mortgage plus home equity borrowing) cannot exceed 80 to 85 percent of your home's value. Use our home equity calculator to run your specific numbers.

Here is a quick example. Your home is worth $450,000. You owe $280,000 on your mortgage. At 85 percent CLTV: ($450,000 times 0.85) minus $280,000 equals $102,500. That is your maximum home equity borrowing. Some lenders go up to 90 percent CLTV but charge higher rates for the additional risk.

The Best Lenders Right Now

For fixed-rate home equity loans, credit unions consistently offer the lowest rates. Navy Federal, PenFed, and local credit unions often beat the big banks by half a percentage point or more. Among the national banks, US Bank and Bank of America have competitive offerings.

For HELOCs, Figure is worth looking at for their fully online process and quick closing, usually under 5 days. Traditional banks like Chase and Wells Fargo offer HELOCs with the advantage of in-person support if you prefer that. Spring EQ and Prosper have expanded their home equity products for borrowers who prefer fintech.

When Home Equity Borrowing Makes Sense

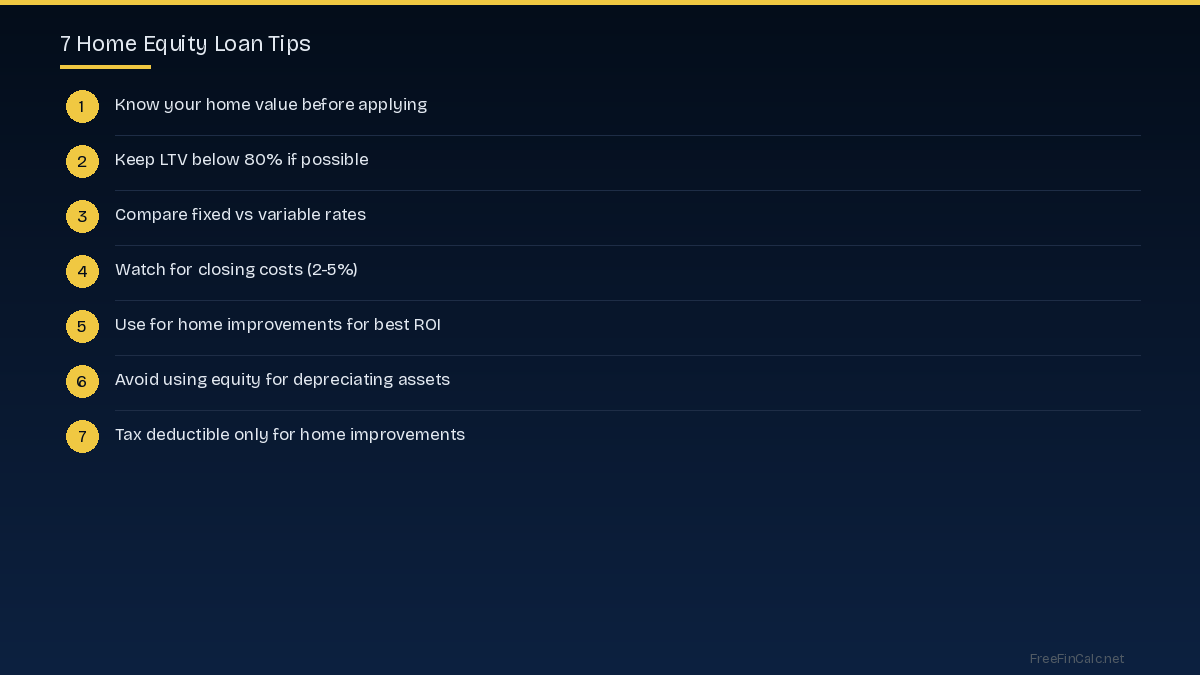

Home improvements that increase your property value are the strongest use case. Kitchen and bathroom renovations, adding a bedroom, or fixing structural issues typically return 60 to 80 percent of their cost in home value. Using equity for these projects essentially lets your home pay for its own upgrades.

Debt consolidation can work if the math is overwhelmingly in your favor. Replacing $30,000 in credit card debt at 22.8 percent with a home equity loan at 8.2 percent saves significant money. But you are converting unsecured debt into debt secured by your home. If you run the credit cards back up, you are in a much worse position than before.

When It Does Not Make Sense

Vacations, cars, weddings, or other depreciating expenses. Borrowing against a 30-year asset to pay for something that loses value immediately is a losing equation. The vacation ends but the debt remains, now attached to your house.

Investing in the stock market. This sounds clever on paper but leveraging your home to invest adds enormous risk. If your investments drop 30 percent in a bad year, you still owe the full amount and your home is the collateral. People lost homes this way in 2008.

If you plan to sell your home within 2 years. Closing costs on home equity products range from 2 to 5 percent of the loan amount. If you sell soon, you will not have enough time to recoup those costs.

The Application Process

Expect it to take 2 to 6 weeks from application to funding. You will need a home appraisal, proof of income, tax returns, and a credit check. Minimum credit scores are typically 680 for the best rates, though some lenders accept 620 with higher rates. Your debt-to-income ratio should be below 43 percent. Use our mortgage calculator to estimate your total monthly obligations.

Shop at least 3 lenders and compare the APR, not just the interest rate. The APR includes closing costs and gives you the true cost of borrowing. Some lenders advertise low rates but load up on fees. Others offer slightly higher rates with no closing costs, which can be cheaper overall for smaller loans.

Tax Implications You Should Know

Under current tax law, home equity loan interest is only deductible if the borrowed funds are used to buy, build, or substantially improve the home securing the loan. If you use a HELOC to remodel your kitchen, the interest is deductible. If you use it to consolidate credit card debt or pay for college, it is not. Keep records of how you spend the money in case of an audit.

The Bottom Line

Home equity is a powerful financial tool but it is not free money. You are borrowing against the roof over your head. Use it for value-adding home improvements or strategic debt consolidation where the math clearly works. Get quotes from at least 3 lenders, compare APRs, and never borrow more than you can comfortably repay even if your income drops. Run your numbers through our refinance calculator to see if a cash-out refi might be a better option for your situation.

Try These Calculators

Frequently Asked Questions

What is the difference between a home equity loan and a HELOC?

A home equity loan gives you a lump sum at a fixed rate with fixed monthly payments, like a second mortgage. A HELOC is a revolving credit line with a variable rate where you borrow as needed during a draw period of 5 to 10 years. HELOCs offer flexibility while home equity loans offer predictability.

How much equity do I need to borrow against my home?

Most lenders require at least 15 to 20 percent equity remaining after the loan. If your home is worth $400,000 and you owe $250,000, you have $150,000 in equity. At 80 percent combined LTV, you could borrow up to $70,000.

Is home equity loan interest tax deductible?

Only if you use the funds to buy, build, or substantially improve the home that secures the loan. Using a home equity loan for debt consolidation, a vacation, or other purposes does not qualify for the interest deduction under current tax law.

What happens if I cannot repay my home equity loan?

Your home is the collateral. If you default, the lender can foreclose, though they are in second position behind your primary mortgage. This makes home equity borrowing riskier than unsecured debt despite the lower interest rates.