Best Personal Loans in 2026: Rates, Lenders and How to Qualify

Updated April 2026 · best personal loans 2026

What a Personal Loan Actually Costs You in 2026

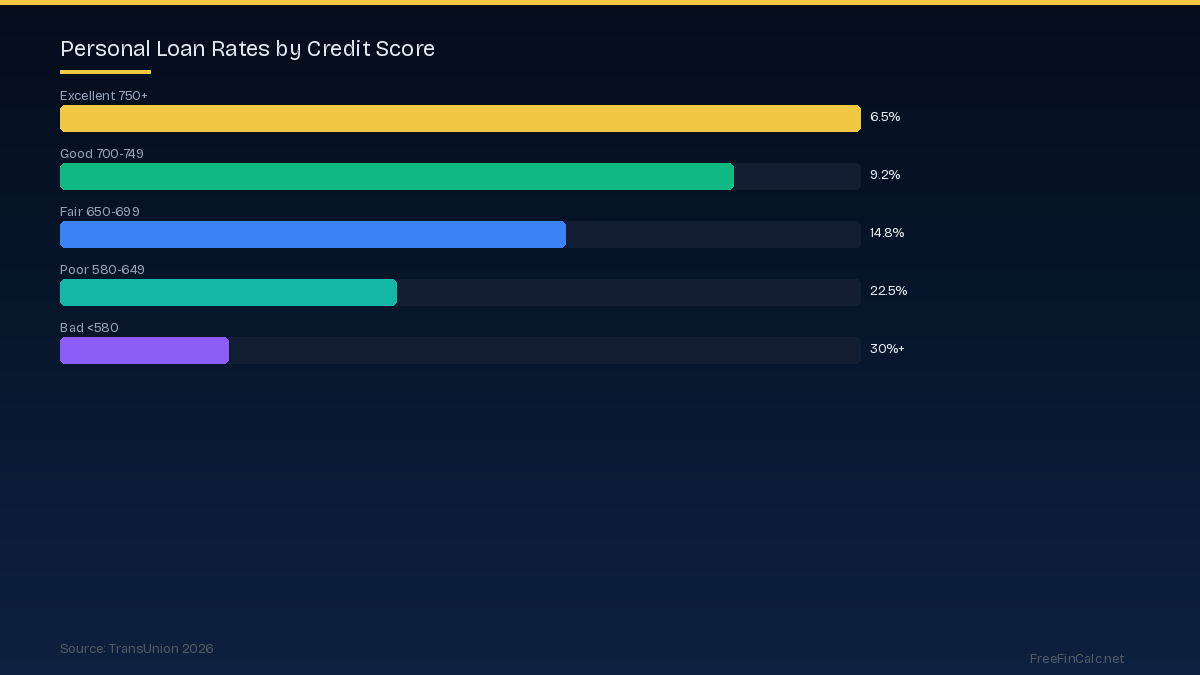

The average personal loan rate right now sits around 8.5% for borrowers with good credit. That is down slightly from 2025 but still well above the pandemic-era lows. For a $15,000 loan over 36 months at 8.5%, you will pay about $1,978 in total interest. Bump that rate to 15% and you are looking at $3,672 in interest on the same loan. The rate you get matters more than most people realize. Credit score is the biggest factor. Here is roughly what you can expect:

Credit score is the biggest factor. Here is roughly what you can expect:Excellent credit (750+): 6.5% to 9% APR. You will get approved almost everywhere and should negotiate.

Good credit (700-749): 9% to 14% APR. Still solid rates. Compare at least four lenders.

Fair credit (650-699): 14% to 20% APR. Credit unions often beat online lenders at this range.

Poor credit (below 650): 20% to 36% APR. Consider whether you actually need the loan at these rates.

Who I Would Actually Borrow From

After comparing 30 lenders, a handful stood out. I am not going to list every single one because most reviews pad their lists with mediocre options to fill space. These are the ones worth your time. For excellent credit, online lenders like LightStream and SoFi consistently offer the lowest rates, often under 7% for well-qualified borrowers. LightStream does not charge origination fees and will fund within a day. SoFi offers unemployment protection, which is a nice safety net. For good credit, Discover and Marcus by Goldman Sachs hit a sweet spot of reasonable rates with no origination fees. Discover lets you pay creditors directly if you are consolidating debt, which removes the temptation to spend the loan on something else. For fair or poor credit, credit unions consistently beat the big banks. The average credit union personal loan rate is about 2 percentage points lower than banks for the same credit profile. If you are not a member of one, many have easy membership requirements.

For fair or poor credit, credit unions consistently beat the big banks. The average credit union personal loan rate is about 2 percentage points lower than banks for the same credit profile. If you are not a member of one, many have easy membership requirements.The Application Process (What Actually Happens)

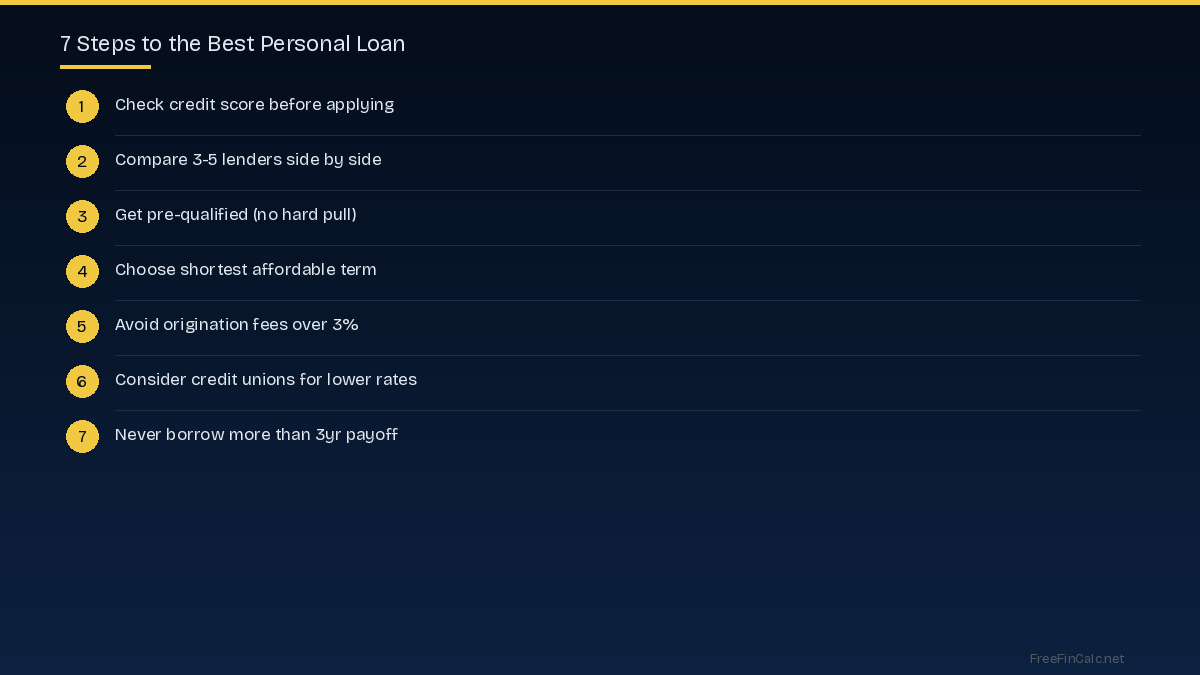

Most people overthink this. Here is the real process: First, check your credit score. You can do this for free through your credit card company, Credit Karma, or AnnualCreditReport.com. Know your number before you apply anywhere. Second, get pre-qualified with 3 to 5 lenders. Pre-qualification uses a soft credit pull, so it will not hurt your score. This takes about 5 minutes per lender and shows you the rate and terms you would actually get. Do not skip this step. The rates advertised on lender websites are the best-case scenario, and you probably will not get the advertised rate. Third, compare the offers side by side. Look at the APR (not just the interest rate), the origination fee if any, the monthly payment, and the total cost of the loan. Our loan comparison calculator makes this easier. Fourth, formally apply with the best offer. This is when the hard credit pull happens. You will need to provide proof of income, employment verification, and a government ID. Most lenders give you a decision within minutes to a few hours.

Origination Fees: The Hidden Cost Nobody Talks About

Some lenders charge an origination fee of 1% to 8% of the loan amount. This gets deducted from your loan proceeds, so if you borrow $10,000 with a 5% fee, you only receive $9,500 but still owe $10,000. That effectively raises your borrowing cost. Here is my rule of thumb: if the origination fee pushes the total cost above what a zero-fee lender offers at a slightly higher rate, skip it. Run the numbers with our personal loan calculator to see the actual difference.Secured vs Unsecured: Which Makes Sense

Most personal loans are unsecured, meaning no collateral required. If you have assets like a savings account or vehicle and want a lower rate, secured loans can save you 2 to 4 percentage points. The trade-off is real though. If you stop paying, the lender takes whatever you put up as collateral. Secured loans make sense when the rate difference is significant and you are confident in your ability to repay. I would not recommend pledging your car for a vacation loan, but using a savings account to secure a debt consolidation loan at 6% instead of 11% unsecured? That math works out.Debt Consolidation: The Most Common Use Case

About 35% of personal loans go toward consolidating existing debt, mostly credit cards. The logic is simple: credit cards average 22.8% APR while personal loans average 8 to 12% for decent credit. Consolidating cuts your rate nearly in half and gives you a fixed payoff date instead of minimum payments that last forever. Here is when it makes sense: if your total credit card debt is above $5,000 and your credit score is at least 670, a consolidation loan will almost certainly save you money. Use our debt consolidation calculator to run the exact numbers. Here is when it does not: if you would run the credit cards back up after paying them off. Be honest with yourself about this. A personal loan does not fix spending habits.

How to Improve Your Rate Before Applying

If your credit score is on the border between tiers (say 695 when 700 would get you a much better rate), it might be worth spending a month or two improving your score first. Quick wins include: Pay down credit card balances below 30% utilization. This can boost your score 20 to 50 points within a billing cycle. Check your credit utilization ratio here. Dispute any errors on your credit report. About 1 in 5 reports contain errors, and fixing them is free. Do not open any new credit accounts or make large purchases on credit in the months before applying. New inquiries and higher balances both drag your score down temporarily. Do not close old credit cards, even if you are not using them. The age of your accounts matters, and closing cards reduces your total available credit, which increases utilization.Red Flags to Watch For

Some personal loan offers are genuinely bad. Watch out for rates above 36% (many states cap rates here, and anything near this ceiling is borderline predatory), mandatory insurance add-ons that inflate the cost, prepayment penalties that charge you for paying early, and lenders that guarantee approval before checking your credit. Legitimate lenders always check credit.The Bottom Line

Getting a good personal loan in 2026 is not complicated, but it does require about an hour of comparison shopping. Check your score, get pre-qualified with a few lenders, compare the total costs, and apply with the best one. For most people with decent credit, you should be able to find rates under 12%. For excellent credit, under 8%. The worst thing you can do is accept the first offer you see or, worse, walk into your bank and take whatever they give you without shopping around. That single hour of comparison could save you $1,000 to $3,000 over the life of the loan. That is a pretty good hourly rate for your time.Try These Calculators

Frequently Asked Questions

What credit score do I need for the best personal loan rates?

For the lowest rates (under 8%), you generally need a credit score of 740 or higher. Scores between 670 and 739 qualify for competitive rates around 10-15%. Some lenders accept scores as low as 580, but expect rates above 20%.

How long does it take to get a personal loan funded?

Most online lenders fund within 1-3 business days after approval. Some offer same-day funding. Traditional banks and credit unions may take 3-7 business days. Pre-qualification usually takes minutes and does not affect your credit score.

Should I get a personal loan to pay off credit card debt?

It often makes sense if your personal loan rate is significantly lower than your credit card APR. The average credit card charges 22.8% while personal loans average 8-12% for good credit. Consolidating saves money and gives you a fixed payoff date.

What is the difference between a secured and unsecured personal loan?

Unsecured loans require no collateral but have higher rates. Secured loans are backed by an asset like a car or savings account, offering lower rates but risking that asset if you default. Most personal loans are unsecured.

Can I get a personal loan with bad credit?

Yes, but expect higher rates (18-36%) and smaller loan amounts. Options include credit union loans, secured personal loans, or co-signed loans. Some online lenders specialize in fair and poor credit borrowers.