How to Get a Business Loan: Requirements, Types and Application Guide (2026)

Updated April 2026 · 12 min read

Business Loan Types: Which One Fits Your Need

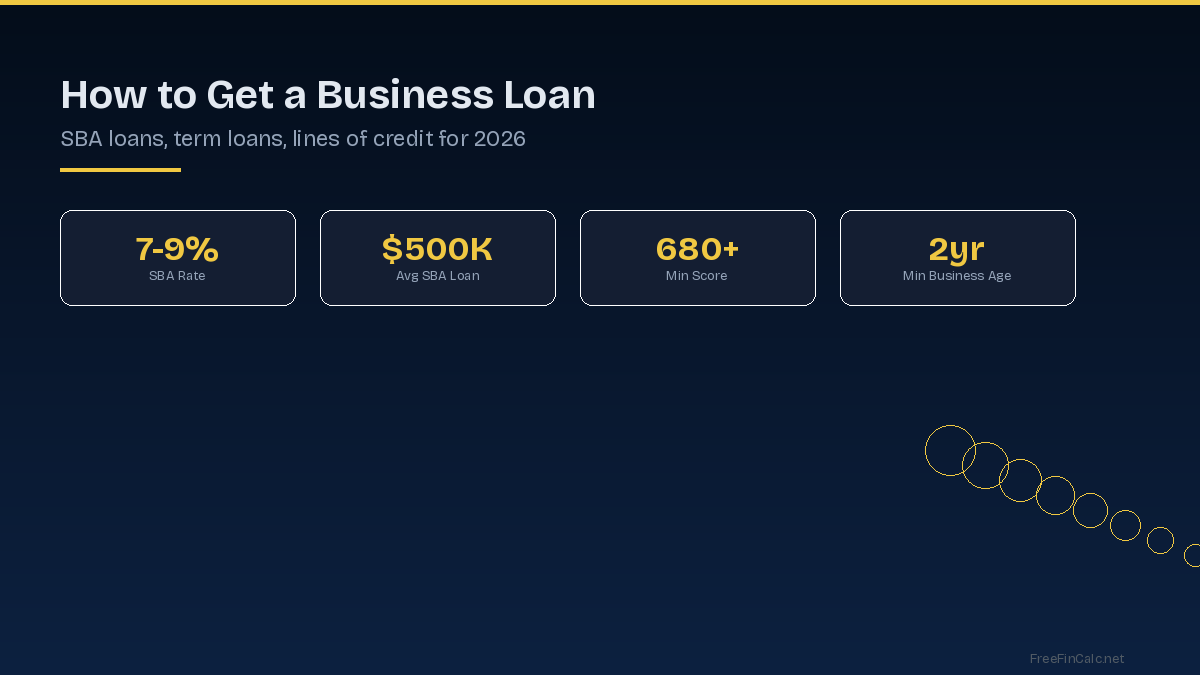

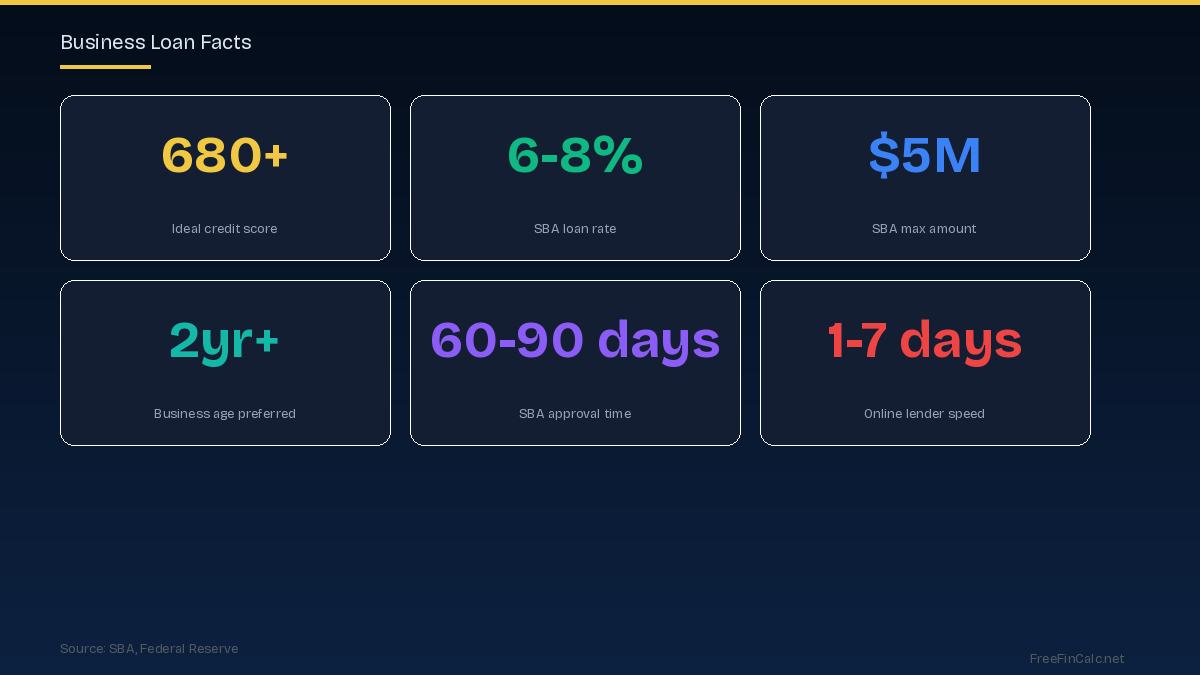

SBA 7(a) Loan: The gold standard. Up to $5 million at 6 to 8 percent interest with terms up to 25 years. Government guarantee means lower rates and easier approval than conventional bank loans. Use for expansion, equipment, working capital, or real estate. Downside: slow process (60-90 days) and significant documentation.

Term Loan: A lump sum repaid in fixed monthly installments over 1 to 10 years. Bank rates: 7 to 15 percent. Online lender rates: 10 to 30 percent. Best for specific one-time expenses like equipment or expansion. Business Line of Credit: Revolving credit you draw from as needed, paying interest only on what you use. Rates: 8 to 24 percent. Best for managing cash flow gaps and unexpected expenses. Equipment Financing: The equipment itself serves as collateral, resulting in lower rates (6 to 12 percent). Best for purchasing machinery, vehicles, or technology.

Calculate your monthly payment with our loan payment calculator before committing to any loan amount and term.

How to Qualify: What Lenders Look For

Personal credit score (680+ for SBA, 700+ for banks). Two or more years in business (startups have limited options). Annual revenue that supports loan payments. A clear business plan showing how the loan will be used and generate return. Collateral for secured loans. Low existing debt relative to revenue.

If your personal credit is below 680, spend 3 to 6 months improving it before applying. The rate difference between 680 and 740 on a $200,000 SBA loan is thousands per year in interest. Build your business credit in parallel by getting a business credit card and paying it in full monthly.

The Application Process Step by Step

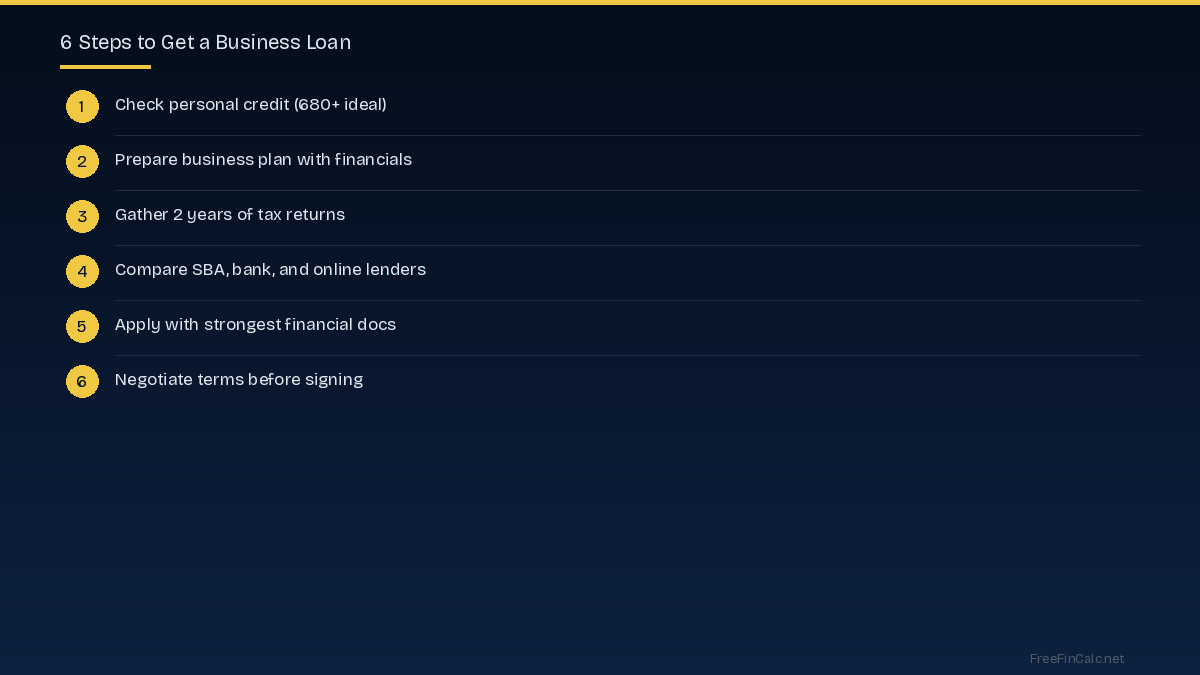

One: determine how much you need and what it is for. Two: check personal and business credit scores. Three: prepare your documentation (business plan, tax returns, bank statements, financial statements). Four: compare SBA lenders, banks, credit unions, and online lenders. Five: apply with the strongest 2 to 3 options. Six: negotiate terms before signing — rates, fees, and prepayment penalties are often flexible. Use our budget planner to ensure the monthly payment fits your business cash flow.

Try These Free Calculators

Frequently Asked Questions

What credit score do I need for a business loan?

SBA loans typically require 680 or higher. Traditional bank loans want 700+. Online lenders accept 580+ but at much higher rates. Your personal credit score matters even for business loans, especially for small businesses without established business credit.

How long does it take to get a business loan?

SBA loans: 60-90 days. Bank term loans: 30-60 days. Online lenders: 1-7 days. The faster the funding, the higher the rate typically. Plan ahead — applying for an SBA loan when you need money urgently means you will end up with a more expensive online loan.

What documents do I need to apply?

Business plan with financial projections, 2-3 years of business and personal tax returns, 6-12 months of bank statements, profit and loss statement, balance sheet, business licenses, and legal documents (articles of incorporation, operating agreement).

What is an SBA loan and why is it the best option?

SBA loans are partially guaranteed by the Small Business Administration, which reduces lender risk and results in lower rates (6-8 percent), longer terms (up to 25 years), and higher approval rates. The SBA 7(a) loan is the most popular, funding up to $5 million for almost any business purpose.

Can I get a business loan for a startup?

It is harder but possible. SBA microloans (up to $50,000) are designed for startups. Online lenders like Kabbage and Fundbox offer smaller loans with less history required. You may need to personally guarantee the loan and provide collateral. Having revenue, even small, dramatically improves your chances.