Best Life Insurance in 2026: Term vs Whole Life, Rates and How Much You Need

Updated April 2026

I have a term life insurance policy. I bought it when my first kid was born, and the whole process took about two weeks from start to finish. The monthly cost is less than my streaming subscriptions combined. That is the thing about life insurance that surprises most people. It is cheap, especially term, and especially if you buy it young.

But the industry makes it confusing on purpose. There are agents who earn massive commissions steering people toward expensive whole life policies when a simple term policy would do the job at a fraction of the cost. Here is what I learned, and what I wish someone had told me before I started shopping.

Term vs Whole Life: The Honest Comparison

Term life insurance covers you for a specific period, usually 10, 20, or 30 years. You pay a fixed monthly premium, and if you die during that term, your beneficiaries get the death benefit. If you outlive the term, the policy expires and you get nothing back. That sounds bad until you realize it is exactly how every other type of insurance works. Your car insurance does not pay out if you never crash.

Whole life insurance covers you for your entire life and includes a cash value component that grows over time. It sounds better on paper, but the premiums are 5 to 15 times higher. A 30 year old male paying $30 per month for a $500,000 term policy would pay $350 to $500 per month for the same coverage as whole life. That difference of $320 or more per month, invested in an index fund at 7 percent, would grow to over $350,000 in 30 years.

The insurance industry will point out that whole life builds cash value. True, but the returns are typically 2 to 4 percent, well below what you would earn in a basic index fund. And the cash value comes with surrender charges if you want to access it in the first 10 to 15 years. It is an expensive way to save money.

How Much Coverage You Actually Need

The rule of thumb is 10 to 12 times your annual income. But rules of thumb are just starting points. The real calculation depends on your specific situation. Use our life insurance calculator to run exact numbers, but here is the framework.

Add up everything your family would need if you died tomorrow: remaining mortgage balance, other debts, future college costs, childcare costs if your partner works, and 5 to 10 years of income replacement. Then subtract assets you already have: existing savings, investments, retirement accounts, and any employer-provided life insurance. The gap is how much additional coverage you need.

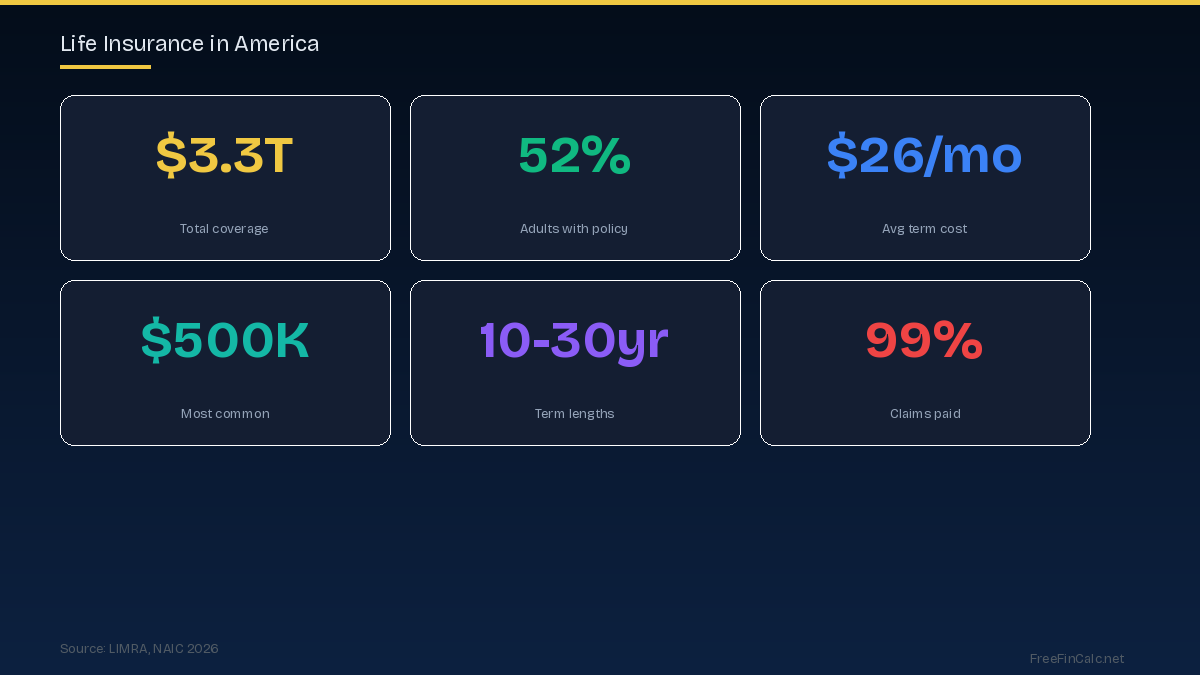

For most families with a mortgage and young kids, this lands between $500,000 and $1,000,000 in coverage. That sounds like a huge number, but a 20-year term policy for that amount costs $25 to $50 per month for a healthy 30 year old.

Where to Get the Best Rates in 2026

The life insurance market has changed a lot in the last five years. Online quote comparison tools have forced transparency, and several companies now offer fully online applications with no medical exam required for healthy applicants under a certain coverage amount.

For the lowest rates, companies like Haven Life (backed by MassMutual), Ladder, and Bestow offer competitive term policies entirely online. Traditional carriers like Northwestern Mutual, State Farm, and New York Life still dominate market share, but their rates tend to be higher for similar coverage. Credit unions sometimes offer group life insurance at discounted rates.

One thing that makes a real difference: get quotes from at least 5 companies. Life insurance pricing varies more than you might expect between carriers because each company weights health factors differently. One company might give you preferred rates despite mild high blood pressure while another charges you standard rates for the same condition.

The Application Process

Traditional life insurance requires a medical exam where a paramedic comes to your home, takes blood and urine samples, and records your height, weight, and blood pressure. Results take 2 to 6 weeks. This is annoying but typically gets you the lowest rates because the insurer has the most data about your health.

No-exam policies skip all that and issue decisions in days or even minutes. The trade-off is rates that run 20 to 40 percent higher, and coverage limits that top out around $500,000 to $1,000,000 depending on the carrier. For healthy people who want the absolute lowest price, the exam route wins. For everyone else, no-exam is a reasonable trade-off.

Common Mistakes That Cost People Money

Buying through your employer only. Group life insurance through work is convenient, but it typically provides just 1 to 2 times your salary, which is not enough. Worse, it usually is not portable. If you leave your job, you lose the coverage, and you will be older and potentially less healthy when you try to buy a new policy.

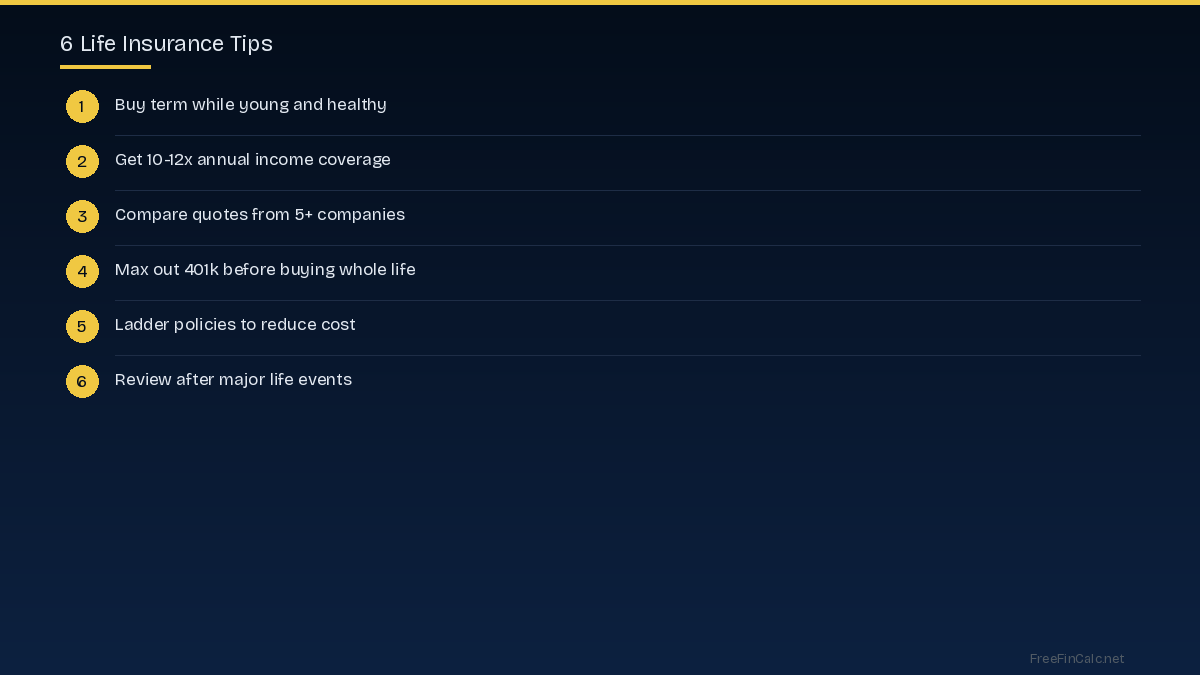

Waiting too long. Every year you delay costs you roughly 8 to 10 percent more in premiums. A healthy 30 year old might pay $22 per month for a 20-year $500,000 term policy. Wait until 40 and that same policy costs $38 per month. Wait until 50 and it jumps to $95. The best time to buy is when you are young and healthy.

Buying whole life when term would do. Unless your net worth exceeds $10 million and you have maxed every tax-advantaged account, term life insurance with the savings invested separately will almost always produce a better financial outcome. Run the numbers with our net worth calculator and retirement calculator to see for yourself.

Policy Riders Worth Considering

Riders are add-ons that customize your policy. Most are unnecessary, but a few provide genuine value. A waiver of premium rider keeps your policy active if you become disabled and cannot work. It typically adds 5 to 10 percent to your premium but can be worth it. An accelerated death benefit rider lets you access part of your death benefit if you are diagnosed with a terminal illness. Many policies include this for free.

A conversion rider lets you convert your term policy to whole life without a new medical exam. This matters if your health deteriorates during your term and you still need coverage after it expires. Most major carriers include some form of conversion privilege, but the specifics vary.

The Bottom Line

Buy term life insurance equal to 10 to 12 times your income. Buy it as young as possible. Get quotes from at least 5 companies. Invest the savings compared to whole life in a low-cost index fund. Review your coverage every 3 to 5 years or after major life events like a new kid, a new house, or a significant salary change. That is the entire strategy, and it works for roughly 95 percent of families.

Try These Calculators

Frequently Asked Questions

How much life insurance do I actually need?

Most financial planners recommend 10 to 12 times your annual income. If you earn $70,000 per year, aim for $700,000 to $840,000 in coverage. Factor in your mortgage balance, other debts, future college costs for kids, and how many years your family would need income replacement.

Is term or whole life insurance better?

Term is better for the vast majority of people. It costs 5 to 15 times less than whole life for the same coverage amount. Whole life only makes sense if you have maxed out all tax-advantaged retirement accounts and need an additional tax-sheltered investment vehicle, which applies to very few people.

Can I get life insurance with a health condition?

Yes. Many conditions like controlled high blood pressure, diabetes, or a history of depression are insurable at higher rates. Some companies specialize in higher-risk applicants. No-exam policies exist but cost 20 to 40 percent more than medically underwritten ones.

At what age should I buy life insurance?

As soon as someone depends on your income. The younger and healthier you are when you buy, the cheaper your rates will be. Rates increase roughly 8 to 10 percent per year of age. A healthy 25 year old pays about half what a healthy 35 year old pays for the same policy.