PPF Calculator India 2026: Interest Rate, Tax Benefits and Maturity Value

Updated April 2026 · 11 min read

Why PPF Is India Best Long-Term Savings Instrument

The Public Provident Fund is the gold standard of safe investing in India. It offers 7.1 percent annual interest that is 100 percent tax-free — no tax on contributions (Section 80C), no tax on interest, no tax on maturity. This EEE (Exempt-Exempt-Exempt) status makes PPF one of only two completely tax-free instruments in India (the other being EPF). At the 30 percent tax bracket, a 7.1 percent tax-free return is equivalent to approximately 10.1 percent pre-tax FD return.

Use our savings calculator to project your PPF maturity value. Investing the maximum Rs 1.5 lakh per year for 15 years at 7.1 percent produces approximately Rs 40.7 lakh at maturity — Rs 18.2 lakh of which is pure tax-free interest. If you extend for another 5 years (block of 5), the corpus crosses Rs 65 lakh.

How to Maximize Your PPF Returns

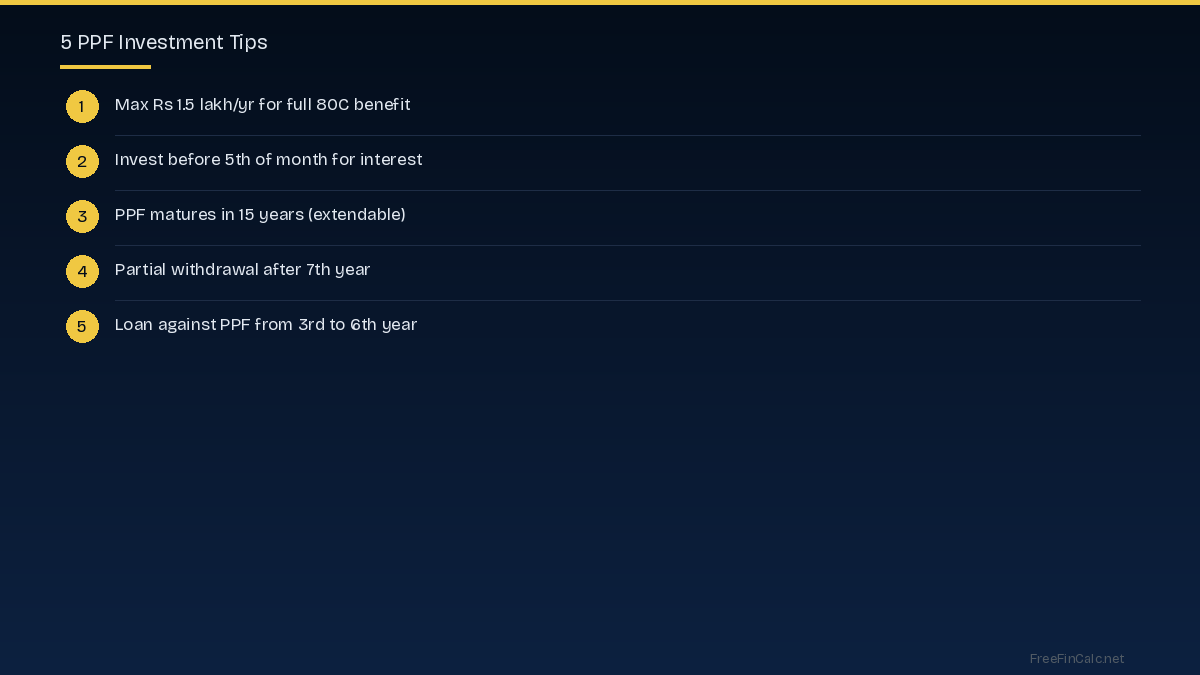

Invest before the 5th of every month. PPF interest is calculated on the minimum balance between the 5th and the last day of each month. If you deposit on the 6th instead of the 4th, you lose an entire month of interest on that deposit. Over 15 years, this timing difference costs you Rs 50,000 to Rs 1 lakh in lost interest.

Invest the full Rs 1.5 lakh every year to maximize the Section 80C deduction. If you cannot invest the full amount at once, set up a monthly standing instruction of Rs 12,500. The minimum annual deposit is only Rs 500 to keep the account active, but investing less than the maximum means leaving tax benefits on the table.

PPF Maturity and Extension Rules

PPF matures after 15 years from the end of the financial year in which you opened it. At maturity you have three options: withdraw the full amount tax-free, extend for 5-year blocks without fresh contributions (existing balance earns interest), or extend for 5-year blocks with fresh contributions (up to Rs 1.5 lakh per year). Most financial advisors recommend extending with contributions if you are still in a taxpaying bracket — the tax-free compounding is too valuable to give up.

Partial withdrawal from the 7th year and loan facility from 3rd to 6th year provide some liquidity during the lock-in period. Use our compound interest calculator and retirement calculator to see how PPF fits into your overall retirement corpus alongside EPF, NPS, and equity investments.

Try These Free Calculators

Frequently Asked Questions

What is the PPF interest rate in 2026?

The current PPF interest rate is 7.1 percent per annum, compounded annually. The rate is set by the government and reviewed quarterly. PPF interest is completely tax-free under the EEE (Exempt-Exempt-Exempt) regime.

How much tax can I save with PPF?

PPF contributions up to Rs 1.5 lakh per year qualify for Section 80C deduction. At the 30 percent tax bracket, this saves Rs 46,800 in taxes annually (including cess). The interest earned and maturity amount are also completely tax-free.

Can I withdraw from PPF before maturity?

Partial withdrawal is allowed from the 7th year onwards, up to 50 percent of the balance at the end of the 4th year or the previous year, whichever is lower. You can also take a loan against PPF from the 3rd to 6th year at 1 percent above PPF rate.

What is the maximum maturity value of PPF?

If you invest the maximum Rs 1.5 lakh every year for 15 years at 7.1 percent, the maturity value is approximately Rs 40.7 lakh (Rs 22.5 lakh invested + Rs 18.2 lakh interest). With 5-year extensions, the corpus grows significantly more.

PPF vs FD: which is better?

PPF wins on tax efficiency (completely tax-free vs FD interest taxed at your slab rate), safety (government guaranteed), and long-term returns (7.1 percent tax-free equals roughly 10 percent pre-tax). FD wins on liquidity (shorter lock-in) and flexibility. For long-term goals, PPF is clearly better.