Mutual Fund Guide India 2026: Types, Best Funds and How to Start

Updated April 2026 · 12 min read

Mutual Fund Categories Explained Simply

India mutual fund industry manages over Rs 65 lakh crore with 44 million investors. If you are not yet investing, you are missing the most accessible wealth-building tool available. Here is what each category means for your money.

Large Cap Funds invest in India top 100 companies (Reliance, TCS, HDFC Bank, Infosys). Return: 10 to 12 percent average. Risk: moderate. Best for: conservative equity investors. Mid Cap Funds invest in companies ranked 101 to 250. Return: 12 to 15 percent. Risk: higher volatility. Best for: investors with 7 or more year horizon. Small Cap Funds invest in companies ranked 251+. Return: 14 to 18 percent in bull markets, can fall 40 to 50 percent in bear markets. Best for: aggressive investors with 10 or more year horizon.

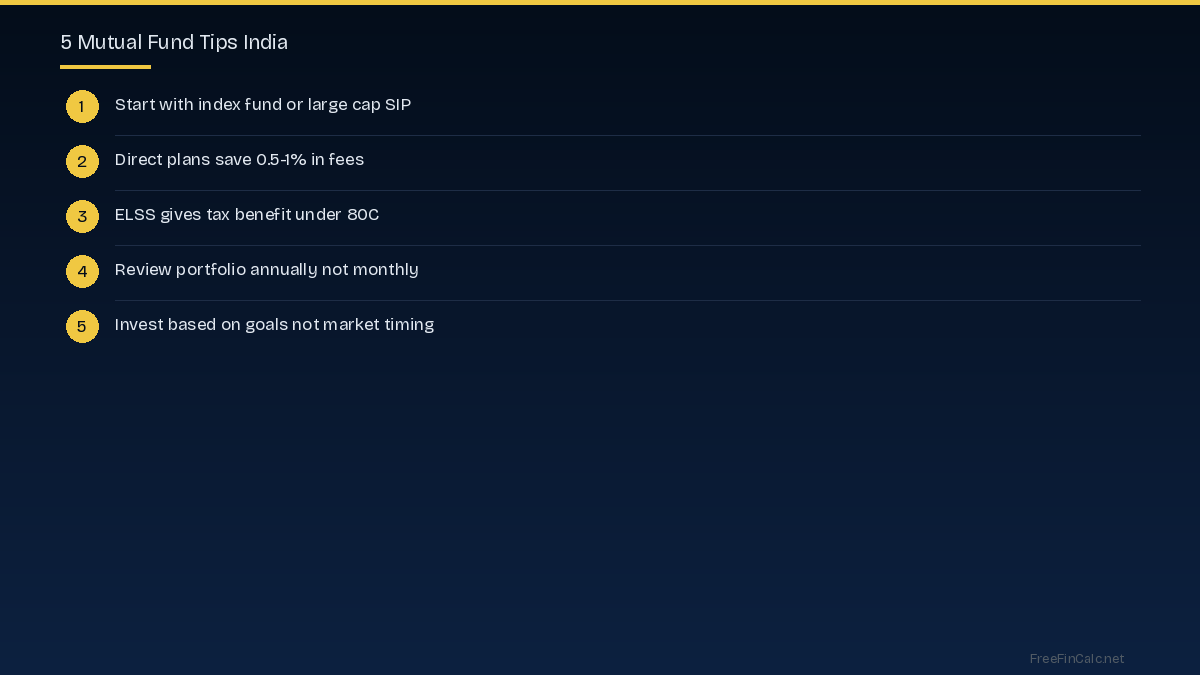

Index Funds passively track the Nifty 50 or Sensex at 0.05 to 0.20 percent expense ratio. Over 10 years, 80 percent of active large cap funds fail to beat the index. This is the single best option for most investors. Use our investment calculator to model returns.

Direct vs Regular: The Rs 20 Lakh Difference

Regular plans pay a commission to distributors (0.5 to 1 percent per year) which comes from your returns. Direct plans do not. On a Rs 10,000 per month SIP for 20 years at 12 percent (direct) versus 11 percent (regular): direct gives Rs 1 crore, regular gives Rs 86 lakh. That 1 percent annual difference costs you Rs 14 lakh over 20 years. Always invest through direct plans on platforms like Kuvera, Groww, or Coin by Zerodha.

The Ideal Mutual Fund Portfolio for Indians

For most people: 60 percent in Nifty 50 index fund, 20 percent in Nifty Next 50 or mid cap index fund, and 20 percent in international fund (Nasdaq 100 or S&P 500). This gives you exposure to Indian large caps, Indian mid caps, and global markets in three simple funds. Add ELSS if you need Section 80C tax deduction. Rebalance annually. Track your portfolio growth with our compound interest calculator and plan your retirement with our retirement calculator.

Try These Free Calculators

Frequently Asked Questions

Which mutual fund is best for beginners in India?

A Nifty 50 index fund through SIP is the best starting point. It gives instant diversification across India top 50 companies at the lowest expense ratio (0.05 to 0.20 percent). UTI Nifty 50, HDFC Nifty 50, and Nippon India Nifty 50 BeES are popular choices.

Are mutual funds safe in India?

Mutual funds are regulated by SEBI and managed by professional fund managers. Your money is held by a custodian, not the AMC, so even if the fund house fails, your investments are protected. However, equity mutual funds carry market risk — NAV can go up or down. Debt funds carry credit and interest rate risk.

How are mutual fund returns taxed in India?

Equity funds: STCG (under 1 year) taxed at 15 percent. LTCG (over 1 year) taxed at 10 percent above Rs 1.25 lakh. Debt funds: taxed at your income tax slab rate regardless of holding period (since 2023 rule change). ELSS provides Section 80C deduction.

What is the difference between direct and regular plans?

Direct plans have lower expense ratios (no distributor commission) and therefore higher returns — typically 0.5 to 1 percent more annually. Over 20 years, this difference compounds to 15 to 20 percent more corpus. Always choose direct plans.

How much should I invest in mutual funds?

At minimum 20 percent of your take-home salary. Start with what you can afford (even Rs 500 per month) and increase by 10 percent every year. The amount matters less than consistency. Someone investing Rs 5,000 per month for 25 years at 12 percent accumulates Rs 95 lakh.