Property Investment in South Africa 2026 — Prices, Bonds & Transfer Duty

Updated April 2026 • South Africa Finance Guide • 8 min read

Overview

South African property remains a cornerstone of wealth building, with the added advantage of no annual property tax (only rates and levies). The market varies significantly by location, with Cape Town commanding the highest premiums.

Key Details

Cape Town prices: Atlantic Seaboard (Camps Bay, Clifton) R5-30M+. Southern Suburbs (Newlands, Claremont) R2-8M. Northern Suburbs (Durbanville, Bellville) R1.5-4M. Cape Winelands (Stellenbosch, Paarl) R2-10M.

Important Considerations

Johannesburg: Sandton R2-10M. Fourways and Bryanston R1.5-5M. Rosebank and Parktown R2-8M. Midrand R800K-2.5M. Soweto and South areas R400K-1.5M.

Additional Information

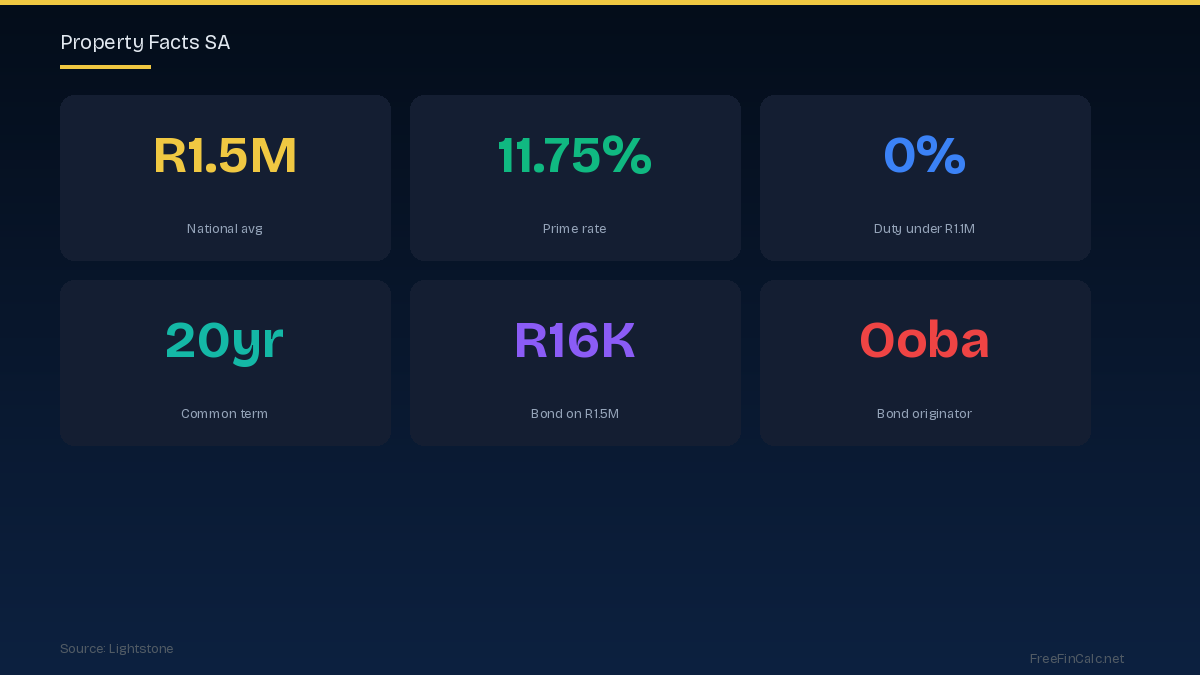

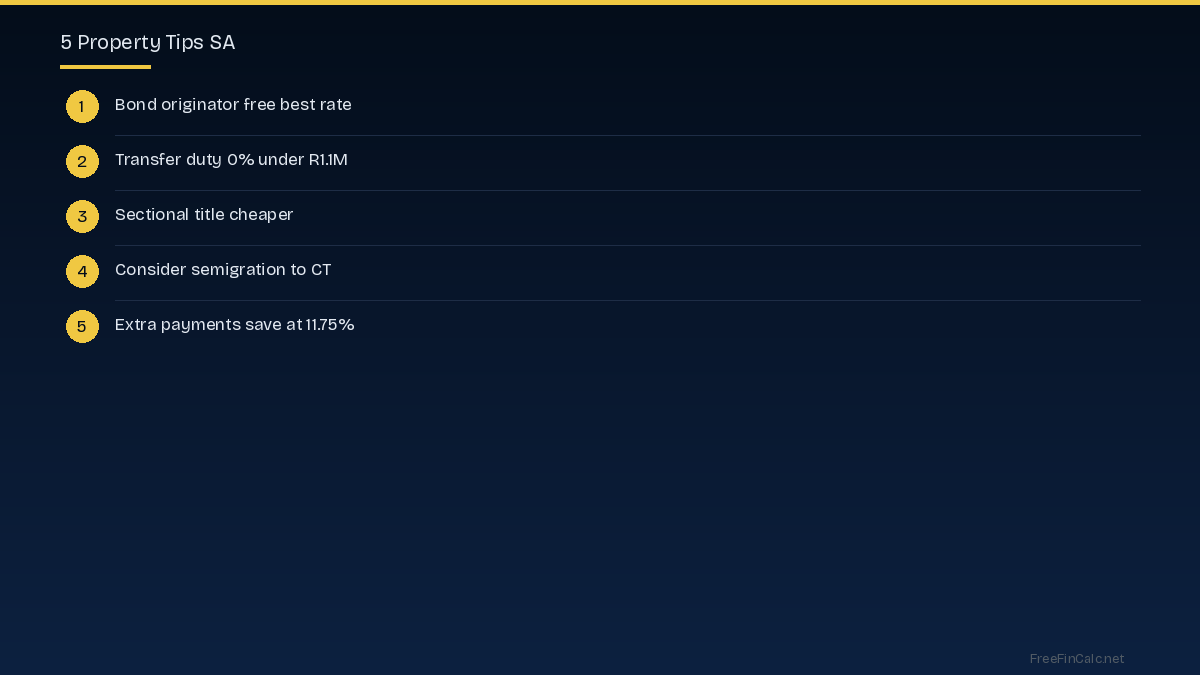

Transfer duty (buyer cost): 0% on properties under R1,100,000. 3% on R1,100,001-R1,512,500. Sliding scale up to 13% on R11M+. First-time buyers benefit most from the zero-rate threshold.

Practical Tips

Bond financing: The prime lending rate is 11.75% as of 2026. On a R1.5M bond over 20 years, monthly repayment is approximately R16,000. Making extra payments of just R1,000/month saves approximately R500,000 in interest and 5 years off the bond term. Use a bond originator like Ooba (free service) to get the best rate from multiple banks simultaneously.

More Information

Sectional title (apartments/townhouses) offers lower entry points than freestanding homes but comes with monthly levies (R1,500-5,000) for communal maintenance and insurance.

Frequently Asked Questions

What is transfer duty in South Africa?

0% under R1.1M. 3% on R1.1-1.5M. Scales up to 13% above R11M. This is a significant buyer cost to budget for.

What is the prime lending rate in SA?

11.75% as of 2026. Most home loans are priced at prime minus 0.25% to plus 2%, depending on your credit profile.

Should I use a bond originator?

Yes, services like Ooba are free (paid by banks) and submit your application to multiple banks simultaneously, getting you the best rate.

How much deposit do I need for a house in SA?

Banks increasingly require 10-20% deposit. 100% bonds are available for strong applicants with good credit and stable income.

Are property prices going up in South Africa?

Cape Town has seen strong growth. Johannesburg is mixed with some areas flat. Interest rate cuts would boost prices. Semigration to Western Cape continues driving CT demand.