Best Savings Accounts in Nigeria 2026 — Rates & Digital Banks

Updated April 2026 • Nigeria Finance Guide • 8 min read

Traditional Bank Savings Rates

The Central Bank of Nigeria sets monetary policy rates influencing commercial bank offerings. As of 2026, most traditional banks offer 3-5% on regular savings accounts. GTBank offers approximately 4.05%, Zenith Bank 3.75%, and Access Bank 3-4.5% depending on balance tier. These rates are significantly below inflation, meaning your purchasing power decreases even while earning interest.

For higher rates, consider fixed deposits. Nigerian banks offer 10-16% on fixed deposits with 90 to 365-day lock-in periods. Heritage Bank and Wema Bank have been competitive with 14-16% on 12-month fixed deposits. The minimum varies from NGN 100,000 to NGN 1,000,000.

Digital Bank and Fintech Savings

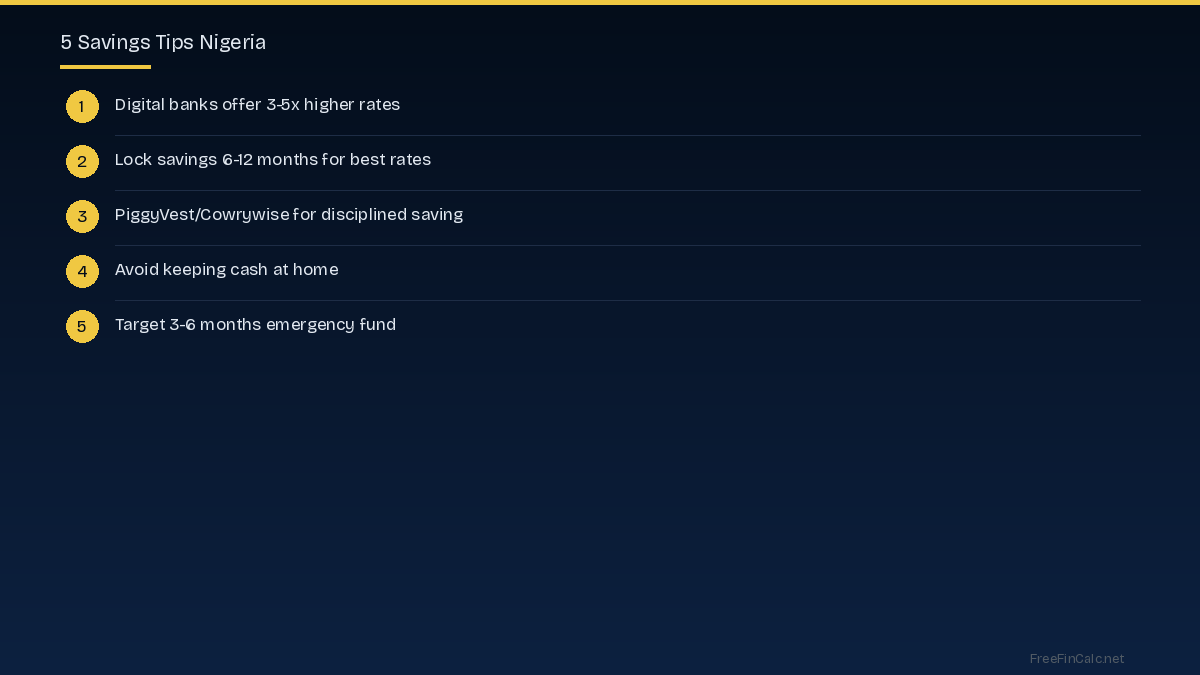

Digital platforms have disrupted Nigerian savings with significantly higher rates. PiggyVest remains the most popular, offering 10-13% on SafeLock savings with terms from 10 days to 24 months. Cowrywise offers similar rates with automatic features. Kuda Bank offers up to 15% on target savings with no minimum balance and free transfers.

OPay has entered the savings space with competitive rates, while Carbon offers savings alongside lending products. All major platforms are CBN-licensed or partner with licensed banks, making them safe up to the NDIC insurance limit of NGN 500,000.

National Savings Certificates

The Federal Government offers savings certificates through the Debt Management Office. FGN Savings Bonds pay quarterly interest and are risk-free since they are backed by the Nigerian government. Treasury Bills offer 10-15% returns for 91, 182, and 364-day maturities, purchasable through commercial banks.

For the best risk-free returns, Treasury Bills remain unmatched. They are available through primary dealers and several fintech platforms now offer direct T-Bill access starting from as little as NGN 1,000.

Money Market Funds

For higher returns with daily liquidity, money market funds are excellent. Stanbic IBTC Money Market Fund, ARM Money Market Fund, and FBN Money Market Fund invest in short-term government securities, offering 10-14% returns with daily access. Minimum investment is typically NGN 5,000-10,000.

How to Maximize Your Savings

Use a tiered approach: keep 1-2 months expenses in regular savings for immediate access, 3-6 months in digital platforms like PiggyVest for your emergency fund, and invest additional savings in T-Bills or money market funds for highest returns. Avoid keeping large amounts in regular bank accounts where 3-5% interest is destroyed by 30%+ inflation.

Also consider diversifying into dollar savings through Risevest or Bamboo. With the naira consistently losing value, even a modest dollar allocation preserves purchasing power over time.

Frequently Asked Questions

What is the best savings rate in Nigeria 2026?

PiggyVest offers 10-13% on locked savings and Kuda up to 15% on target savings. Traditional banks only offer 3-5% on regular savings.

Is PiggyVest safe for saving money?

Yes, PiggyVest is SEC-licensed and partners with CBN-licensed banks. Deposits are insured by NDIC up to NGN 500,000. Over 4 million Nigerians use it.

How much should I save monthly in Nigeria?

Save at least 20% of monthly income. For someone earning NGN 200,000, that is NGN 40,000/month. Start small and increase gradually.

Are digital banks safe in Nigeria?

CBN-licensed digital banks like Kuda, OPay, and Moniepoint are safe. Always verify licensing. Deposits insured up to NGN 500,000 by NDIC.

What is the NDIC insurance limit?

NDIC insures deposits up to NGN 500,000 per depositor per commercial bank and NGN 200,000 for microfinance banks.