Retirement Planning in South Africa 2026 — RA, TFSA & Two-Pot System

Updated April 2026 • South Africa Finance Guide • 8 min read

Overview

Retirement planning in South Africa requires navigating several savings vehicles, each with different tax treatment and access rules. The introduction of the two-pot system in September 2024 fundamentally changed how retirement savings work.

Key Details

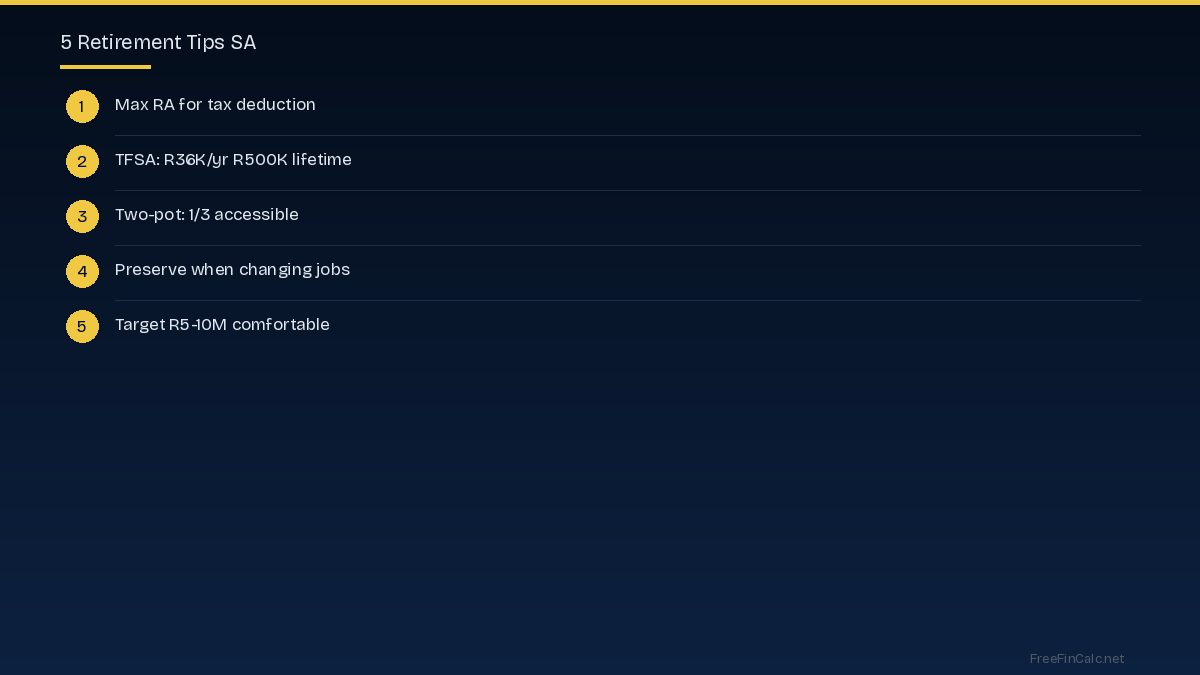

Retirement Annuity (RA) is the most tax-efficient savings vehicle. Contributions are deductible up to 27.5% of taxable income (max R350K). Growth is tax-free. At retirement (earliest age 55), you can take one-third as a lump sum (first R550,000 tax-free) and must use two-thirds to purchase an annuity providing monthly income.

Important Considerations

Tax-Free Savings Account (TFSA) allows R36,000 per year (R500,000 lifetime) with all growth completely tax-free. Unlike RA, there are no restrictions on withdrawals, but you lose the contribution room if you withdraw. Best strategy: invest in equity ETFs for maximum long-term growth.

Additional Information

Two-pot retirement system (from September 2024): One-third of new contributions go into a savings pot (accessible once per year, taxed at marginal rate), two-thirds into a retirement pot (locked until retirement). This provides limited emergency access while protecting most retirement savings.

Practical Tips

How much do you need to retire in SA? Financial planners typically recommend 15-17x your annual expenses. For a R30,000/month lifestyle, you need approximately R5.4-6.1 million. For R50,000/month, target R9-10.2 million. The earlier you start, the less you need to save monthly due to compound growth.

Frequently Asked Questions

How much do I need to retire in South Africa?

Target 15-17x annual expenses. For R30K/month lifestyle: R5.4-6.1M. For R50K/month: R9-10.2M.

What is the two-pot retirement system?

From September 2024: 1/3 of new contributions go to an accessible savings pot, 2/3 to a locked retirement pot. Savings pot accessible once per year, taxed at marginal rate.

What is the TFSA annual limit?

R36,000 per year with a R500,000 lifetime limit. All growth is completely tax-free.

When can I access my RA?

Earliest at age 55. You can take 1/3 as lump sum (first R550K tax-free) and must annuitize the remaining 2/3 for monthly income.

Should I choose RA or TFSA?

Both. Max TFSA first (R36K/yr) for flexible tax-free savings, then contribute to RA for the tax deduction benefit on additional savings.