TFSA Guide South Africa 2026 — Tax-Free Savings Account Rules & Strategy

Updated April 2026 • South Africa Finance Guide • 8 min read

Overview

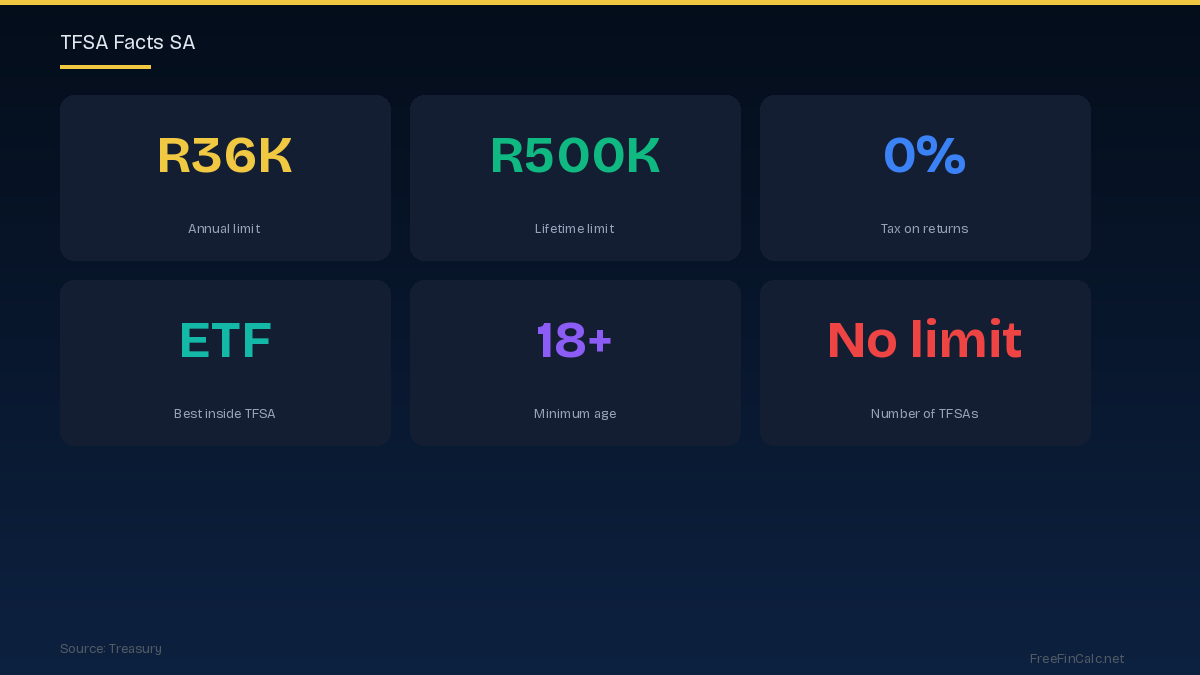

The Tax-Free Savings Account is one of the most powerful wealth-building tools available to South Africans. Every rand of growth — interest, dividends, and capital gains — is completely tax-free. If you are not maximizing your TFSA, you are leaving money on the table.

Key Details

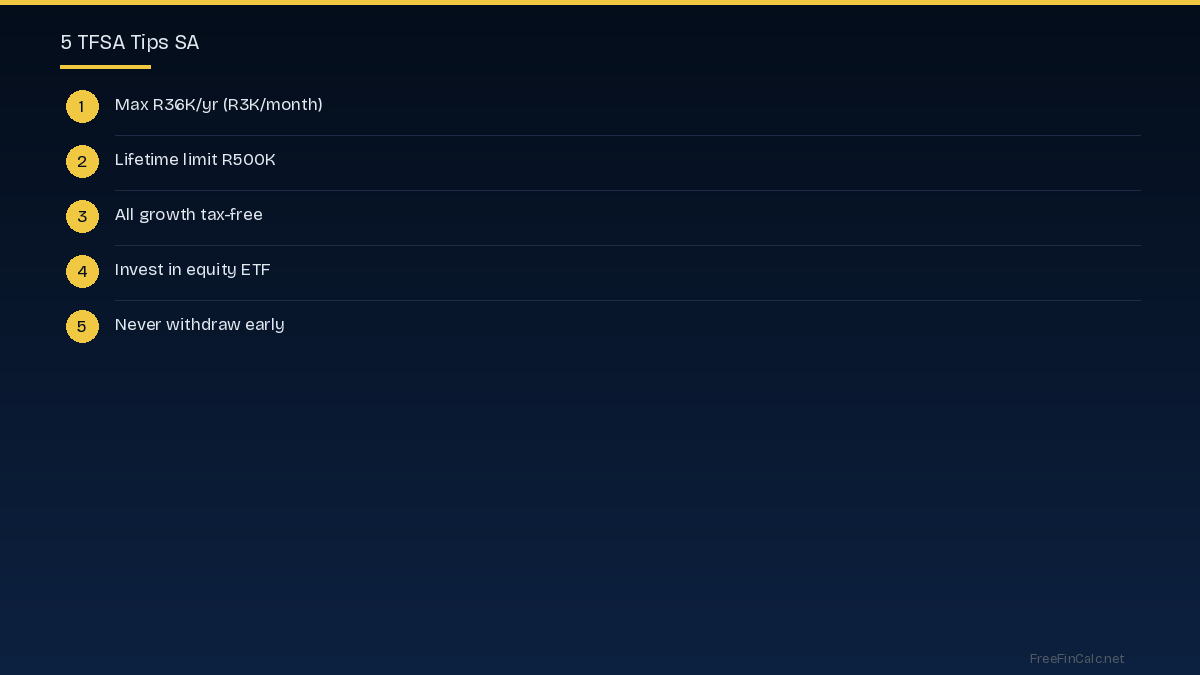

Rules: Maximum R36,000 per year (R3,000/month). Lifetime limit of R500,000. No restrictions on number of TFSAs. Available to anyone 18+ with a South African ID. You can withdraw at any time, but you lose that contribution space permanently — it does not reset.

Important Considerations

Where to open a TFSA: EasyEquities offers the lowest fees with zero minimums. Satrix offers direct ETF investment. Allan Gray, Coronation, and Sygnia offer TFSA wrappers around their unit trust funds. Most South African banks also offer TFSAs but typically with lower returns.

Additional Information

Best investments inside a TFSA: Since growth is tax-free, maximize growth potential with equity ETFs. Satrix Top 40 for SA equity exposure (0.10% TER). Satrix MSCI World for global equity (0.35% TER). A 50/50 split between local and global equities provides diversification. Avoid holding cash or bonds inside a TFSA — the tax benefit is wasted on low-growth assets.

Practical Tips

Long-term impact: Contributing R36,000 per year for 30 years at 10% average return grows to approximately R6.5 million — all completely tax-free. The equivalent in a taxable account would be worth significantly less after dividend tax, interest tax, and capital gains tax.

Frequently Asked Questions

What is the TFSA annual limit in South Africa?

R36,000 per year (R3,000 per month). Lifetime limit is R500,000.

Is TFSA really tax-free?

Yes, all returns inside a TFSA — interest, dividends, and capital gains — are 100% tax-free. No tax on growth or withdrawal.

What is the best investment for TFSA?

Equity ETFs like Satrix Top 40 (SA) and Satrix MSCI World (global). Maximize growth since tax-free status benefits high-growth assets most.

Can I withdraw from my TFSA?

Yes, anytime without penalty. However, you permanently lose that contribution space — it does not reset the following year.

Where should I open a TFSA?

EasyEquities (lowest fees, no minimum), Satrix (direct ETF), or Allan Gray (unit trust). Compare fees as they compound significantly over time.